This one is for the idea people out there. Some will scream scam and others will find intrigue. I’m part of the latter and believe the topic of this article stands out as one of the more fascinating examples of DeFi’s innovation and potential as a disruptor, regardless of long-term survival. Lasting concepts like protocol-owned liquidity all have their roots here, so it is an important one to understand.

The protocol is Olympus DAO, which launched in 2021 and ultimately gave rise to countless forks which more or less copied its model. Read on for some history on how this protocol was able to capture the imaginations of countless individuals while also soon falling from grace nearly as fast as it rose. There’s a famous paradox that says that the seeds of success may lead to one’s own demise — truer words may never have been spoken.

Through this piece I also hope to provide a taste of the brazen innovation that is occurring more broadly across the industry. These are bold and untested ideas of great scope, and Olympus is but one example among many that either already have or will soon make an impact one way or another. Few industries can say the same, making it such an exciting space to follow at this stage of development.

DeFi’s Problem With Stablecoins

Olympus DAO was created in part to solve Web3’s reliance on centralized stablecoins. See below for background on DeFi’s “problem” and the grand idea proposed to address it.

Centralized Stablecoins

Most of us are pretty familiar with the concept of stablecoins by now. Although they come in various forms, these are traditionally asset-backed tokens whose value is pegged to real-world asset classes like fiat currencies or commodities. For example, each of Tether ($USDT) and USD Coin ($USDC) are pegged to the U.S. dollar and are meant to maintain an equivalent value to the USD at all times (i.e., 1 USDT = $1). To accomplish this peg each of these coins are theoretically backed 1-for-1 with U.S. dollars or a near-equivalent such as short-term Treasuries to serve as collateral. Although clearly not riveting in terms of return potential, stablecoins are some of the most widely held tokens and play an important role in the broader crypto ecosystem by offering investors stability in an otherwise volatile end market without having to rotate into hard cash and deal with related pain points like time-consuming bank transfers.

A Bold Solution Emerges

Despite the key role stablecoins play in the proper functioning of the broader crypto ecosystem, this doesn’t mean stables are without their own flaws from a DeFi perspective. For one, these tokens are centralized and depend on other actors to operate — e.g., USDC is managed by a consortium called Centre (which was co-founded by Circle and Coinbase) who is responsible for maintaining the coin’s peg with adequate collateral/reserves. Additionally, since pegged to the dollar, this also means USDT and USDC are inherently subject to a depreciating dollar which is influenced by the monetary policies of the United States. You can probably see how these attributes do not sit well with decentralized purists.

As a result, an entirely new concept emerged. What if instead of relying on centralized tokens like USDC that are almost entirely backed by USD and other traditional assets, a Web3-native currency or stablecoin not dependent on fiat currency pegs or the whims of government policy emerged as the liquid gold standard used and held across the decentralized ecosystem as a unit of account? A cool concept for sure, but could it work?

A Decentralized Alternative

Olympus DAO was the first to introduce the concept described in the previous section, calling for a “decentralized reserve currency” to be utilized across all of Web3. Whereas the U.S. dollar is the world’s dominant reserve currency held by central banks and major financial institutions across the world (for things like international trade, settlement, etc.), Olympus DAO seeks to have its own crypto-native token ($OHM) serve a similar function across the DeFi ecosystem. This means providing the growing Web3 financial system with a relatively stable, censorship-resistant currency that has deep liquidity and is trusted and used widely across different platforms and chains (among other things).

The above might all sound great, but how in the world was Olympus able to go about implementing its vision? This is where both innovation and a bit of controversy come into play.

(1) Amassing a Treasury / Protocol-Owned Liquidity

First — how to amass a treasury of other assets to back OHM and get the project off the ground?

To accomplish this, rather than going the traditional route via VC funding or other means, Olympus implemented a novel “bonding mechanism” to bootstrap liquidity for the protocol. Think of Olympus bonds as a type of original issue discount (OID) bond, which as the name implies are issued at a discount to face value. Here, bonding allows users to buy OHM tokens at a discount. If, for example, OHM costs $500 on the open market, users can purchase that same token for $450 through the bonding mechanism. After a period of time (~5 days), users can then withdraw the full $500 worth of OHM that they paid $450 for. The vesting period is required or else immediate arbitrage would be available — just like for traditional OIDs.

Since OHM was cheaper as a bond than in the open market, there was incentive for users to forego secondary trading (where gain/loss only passes through between counterparties) and instead purchase the token directly from the protocol via bonding. This process allowed Olympus to take in outside liquidity from users in exchange for newly minted OHM, growing its internal treasury in the process. It’s analogous to how a reserve bank (Olympus here) might sell its country’s currency (which it controls) for foreign currency in the open market, which it then stores away.

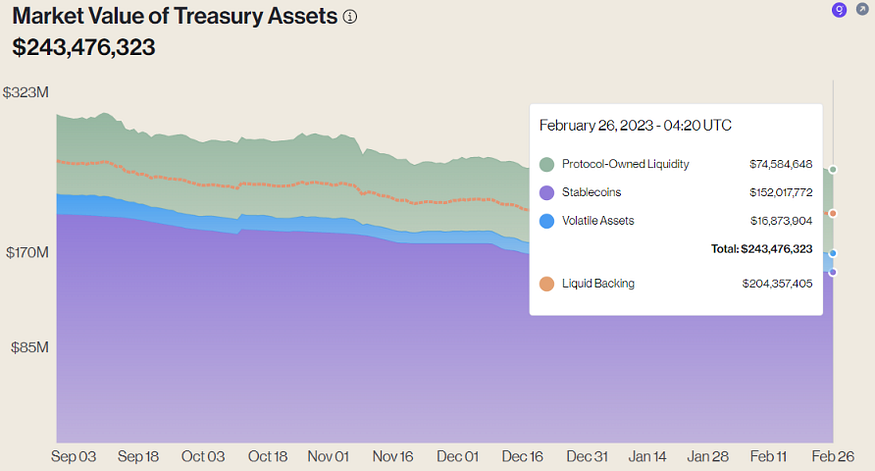

Not surprisingly, the success Olympus ultimately had in raising hundreds of millions of dollars in treasury essentially out of thin air from this process was captivating and pioneered what is known as ‘protocol-owned liquidity.’ This is an important concept and may potentially serve as Olympus’ most lasting impact on DeFi. Read here for a nice primer on the topic, in particular how it’s used to help resolve mercenary liquidity problems that many decentralized tokens face.

In short, Olympus was able to use a portion of treasury assets raised to provide liquidity to OHM trading pairs on decentralized exchanges (DEXs). Most tokens need to rent liquidity on DEXs by enticing users to deposit into their liquidity pools with attractive yield rewards. However, by acting as its own liquidity provider, OHM trading pairs were no longer fully reliant on other yield farmers. For a project seeking to become a decentralized reserve currency used broadly across the ecosystem, being able to ensure liquidity and stability in this way was an important part of maintaining trust in the function of the token. And this ability all came about through Olympus’ innovative way to raise capital for its treasury, which depended on nobody but the trust of those bonding.

(2) Creating Demand for OHM

Now for the controversy. It’s great that someone can buy OHM at a discount via bonding, but if OHM is worthless who cares to do it? This was another big piece of the puzzle. Olympus DAO figured out the mechanism through which it could bootstrap liquidity (described above), but without demand for OHM which incentivizes bonding, the project’s strategy for building its treasury falls apart.

The solution — offer eye-watering APY returns for staking OHM to bring hungry investors in. For example, when the protocol first launched, it was offering six-digit APYs (100,000%+) on staked OHM. This means that if you purchased and staked (i.e., locked up) 1 OHM, compounded over the course of a year you would have 1000 OHM by year end. You have my attention.

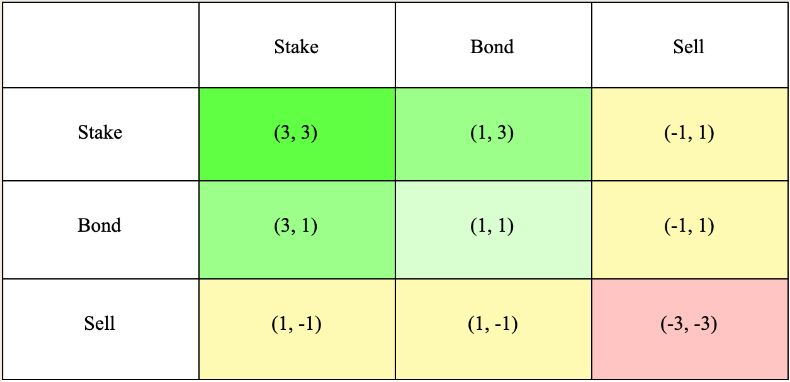

Key point though — this is 1000 OHM, not dollars. To pay out this APY the protocol issues new OHM, thus simultaneously diluting the value of OHM in the process (i.e., true value isn’t created, just like with stock splits). However, the novelty of the high APY still attracted many investors, and since the only way to claim these rewards was to have OHM staked within the protocol (historically 90%+ of OHM was staked), a large portion of the asset supply was locked up, further supporting price and incentivizing demand. This construct is where Olympus’ famous game theory tag (3,3) arose. Given three options between two investors — stake, bond or sell — the dominant strategy in terms of value would be for both sides to stake OHM (higher OHM price + more OHM in pocket for all).

Is this Ponzi-esque? It is, and did not end up being sustainable for long as APYs eventually came down quickly (read the next section as to why this was unsustainable given OHM’s required backing). Many uninformed investors were also probably confused and/or deceived by promises of value here, which is not good. When Olympus DAO is brought up in conversations or by the media, it’s these sky-high APYs that are highlighted. I’m not defending them in any way, but merely wish to highlight the fact that these were levers used as part of a broader strategy — to stir demand for OHM, which indirectly enabled the protocol to bootstrap liquidity through bonding in order to pursue its core mission. Looking at the high APYs in isolation from Olympus’ greater goals and lasting impact on Web3 does not do the project full justice. Others may disagree.

Ponzi or not, for some early investors in OHM, the returns were absolutely astronomical. Not only did some investors receive high five figure or even six figure APYs over a few months, but the price of OHM itself went from the low $100s to over $1500 per OHM during the same period. Here’s an article highlighting how one early investor turned $500 into nearly $5 million at its peak riding the wave.

(3) Backed…But Not Pegged

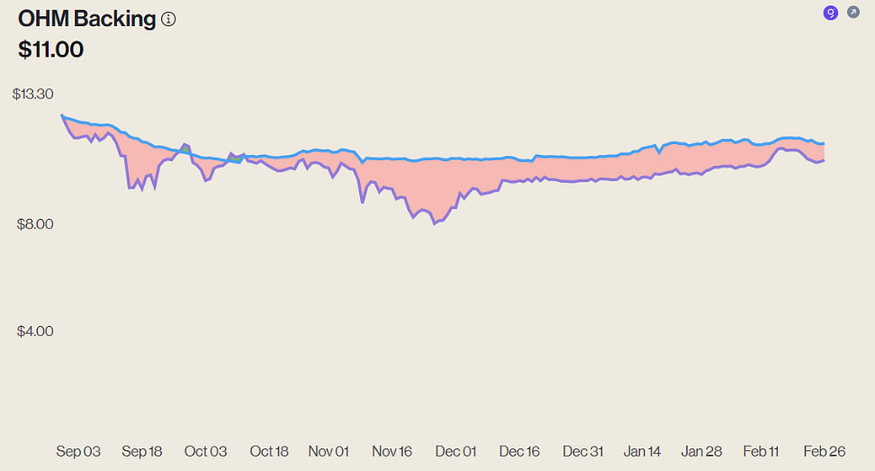

Lastly, you may have noticed that OHM’s price is neither stable nor pegged to any other fixed value. Rather, the token can fluctuate in price as determined by the market, with a theoretical floor value of $1. Although this set up is a big difference from stablecoins like USDT and USDC, the floor value is meant to provide a higher degree of security and trust compared to other freely tradable assets that might seek to play the same role as OHM.

The floor value is due to each OHM being backed, but not pegged, by at least $1 worth of assets in the Olympus treasury. Think pegged == $1, while backed >= $1. So, if there are 100 million OHM tokens in circulation, there should be at least $100 million worth of assets in Olympus’ treasury at all times to maintain a floor. On the other hand, OHM could always trade above $1 because there is no upper limit imposed by the protocol.

You might be asking — what prevents Olympus’ treasury from depreciating in value and unexpectedly lowering the backing price below $1? It’s a good question and an inherent risk since the treasury contains both stablecoins like FRAX and DAI as well as volatile assets like ETH. It’s also the reason why there is currently a cushion in terms of treasury vs. float to help prevent against this should calamity arise (i.e., the token is at ~$10 despite technically trading below backing). Additionally, if the token’s supply were not managed properly and kept in check by eventually lowering the ridiculous APYs described before, supply could easily outpace the treasury’s backing and destroy the floor. The treasury-to-float ratio is thus very important for Olympus to manage or else risk losing trust in OHM’s long-term value proposition.

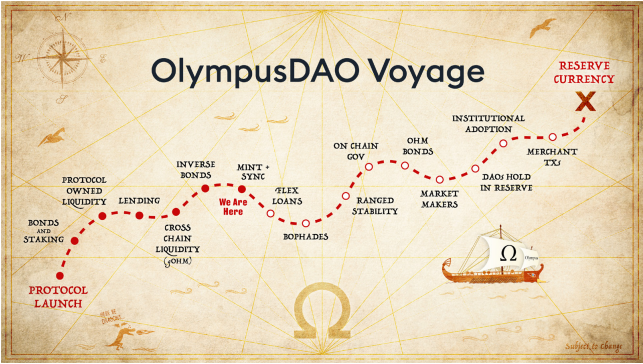

Conclusion / Olympus DAO Today

In case you’re wondering, Olympus DAO is still around today — read here for its Q4 2022 Report which provides recent updates and ongoings. Growth first, stability later. That was Olympus’ motto, as without the former there would never be a future to stand on.

Whether Olympus is ever able to fully mature out of its growth phase and achieve its end goal as a widely used decentralized reserve currency is unknown, and partly depends on how well the DAO utilizes and manages its treasury moving forward. Some initiatives are still forthcoming (see below roadmap), and the protocol continues to make efforts to build partnerships across the Web3 ecosystem which are meant to improve OHM’s integration within it.

But there is also no getting around the elephant in the room — since first launching, OHM’s price has cratered and burnt many investors in the process, some of whom feel deceived by promises of high APYs. Ironically though, the price decline was largely by design. During the protocol’s early phase, speculation was both expected and also needed for growth. However, over time as the project scaled, the speculative component was anticipated to diminish, with price eventually converging toward backing. Whether investors fully grasped this dynamic, who knows. But for a project depending on the collective belief of those in the ecosystem in order to succeed, it’s a dangerous game to play for original supporters to turn sour and never return.

References

- The Future Decentralized Reserve Currency

- Olympus DAO — The Decentralized Reserve Currency

- Why DeFi Projects Are Flocking to Olympus DAO Bonding

- Olympus DAO: DeFi’s Answer to Mercenary Liquidity

- The Battle for Liquidity: Analyzing Olympus, Wonderland, and Redacted

- What Is a Stablecoin?

- What is Protocol-Owned Liquidity? A Primer on the Model Developed by Olympus DAO

- No One Understands Olympus DAO

Comments ()